How to Crush Your Budgeting Blues and Finally Enjoy That Dream Family Vacation

How to Crush Your Budgeting Blues and Finally Enjoy That Dream Family Vacation

It's not about restricting you. It's about giving you control

When people first hear the word “budget”, they think of penny-pinching every cent.

They have all these ideas of how restricting it is. Aren’t people who make budgets and the old lady with a thousand coupons at the grocery store the same people?

No, they are usually the exact opposite.

While poor people tend to use a one-time coupon or a code for a 10% discount, rich people watch their money 24/7. They are not as concerned with the coupons as they are with their finance strategy.

That’s where the budget comes in. budgeting is all about keeping track of your money and making sure you know where every dollar is going. It allows you to control your money, not the other way around.

People think that they’ll need to give up everything they love to live by a budget. No more going out to eat. No more going shopping for clothes or shoes. No more milk bones for the beloved family dog.

This is not the way it has to be. You need to be more aware of how much you’re spending in each category.

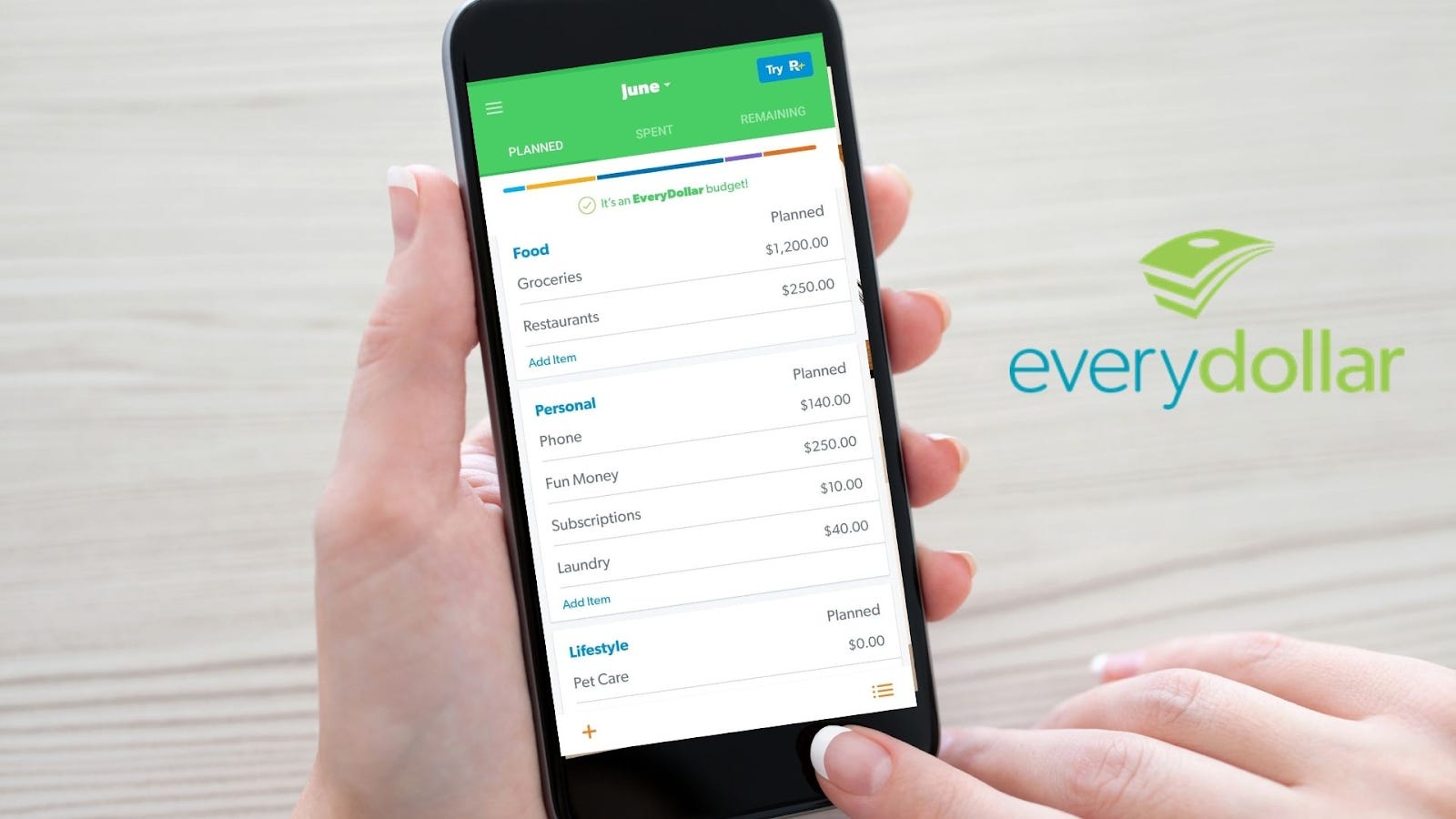

While you could do this by hand or in the notes app on your phone, there’s a better way. There are a million apps to choose from, but the one I use is called EveryDollar (I have no affiliation with them).

Created by Dave Ramsey and his team, the app is simple and free (with paid features if you want them). The free version is perfect. It has everything you need to get started.

As the name implies, you'll be tracking every dollar that comes in and goes out. You’ll start by adding how much you get paid a month. This includes all your income sources. This could be paychecks, child support, rental income, etc.

It then lists several groups of categories that you can add or subtract items from. Check out the photo below.

As you can see under the personal tab, there are four different subsections you can add. You can add as many as you want, so make sure to include everything. You then enter the dollar amount you expect to spend on that item every month.

The goal at the end of the budget is to make sure that your entire income for the month minus your total expenses equal zero.

For example, let's say you make $5,000 a month. after you have finished entering your expenses, you should have $0.

One of your categories is called savings. Underneath it, you can list the subcategories. For example, you could have a regular savings goal you want to hit each month. You could add a separate section called "vacation savings" to plan for your trip to Italy one year from now.

You want to have money directed to savings. it's a category so you know how much you save monthly.

The budget is you telling your money where to go. Every dollar has a task and a job to do. Your budget puts you in charge of your money.

If you're like me, you have all your income deposited into your checking account. At the end of the month, I like to take the savings I have each month and move them to my savings account.

It's nice to see the savings account grow every month. If you are consistent with this, you will see how fast your savings account grows. Even if you save $100 a month, 5 months go by quickly and you’ll have a cool $500 to give you some breathing room.

Remember, you don’t have to cut out eating at restaurants entirely. You need to be clear on how much you are willing to spend.

When I was first starting, I couldn’t believe the amount of money I spent on going out to eat. Everything from sit-down restaurants to fast food, I would hit the $300+ range every month.

Your budget will open your eyes to your spending habits. It will show the good, the bad, and the ugly.

Now you might be thinking this sounds great, but what if I can’t save anything?

You need to dig deep and take a hard look in the mirror. Do you have an iPhone? Do you go out with friends to the mall or for drinks? Do you pay for Netflix?

These are nonessential. If you can’t afford to put any money away or pay off debts, these should be the first cuts to make.

Even with all this, you may still not have enough to save or pay off your student loans and credit cards.

What then?

If you are breaking even every month (or going deeper into debt), you need to raise your income. If there is no room to make cuts, you need to make more money.

You have to figure out how to do this on your own. Some of the more obvious choices are as follows. You can work more hours at your current job, work a part-time job on the weekends, do something like Door Dash, and more.

Working more hours at your current job is best if you can. You would receive overtime pay and are already familiar and comfortable with the work.

If you don’t decide to do anything now, what is your life going to look like in five years? If you don’t do anything different, then you will have the same problems.

Everyone knows about inflation. It’s only going to get worse as the years go on. There is no better time to control your finances than right now.

The budget is key. It's your blueprint to give you absolute control over your money. The budget is the plan you need to start saving or paying off your debt.

It will be hard to do at first. You might have a hard time figuring out exactly how much you spend a month. You should look at your bank history and find any recurring payments every month.

This would include things like your rent/mortgage payment, electricity, phone bill, wifi, etc. Once you know what's constant every month, you can work on the things that may vary.

If your pay tends to deviate, start with the lower expected amount. This will avoid major changes to the budget should you not receive the higher amount.

Once you work at this for a month or two, you’ll have a much clearer picture of how much you spend and where.

Then it's all rinse and repeat.

You'll be glad you started when you did!